If you think of retirement planning as a game, it’s a slippery one—rules shift mid-play, sometimes favoring you, sometimes blind-siding you when you least expect it. You’re jogging along, aiming for a finish line, but suddenly the clock resets or the boundaries move. More time to save. Fewer perks. A tax code sleight of hand just as you’re getting your bearings. What someone needs now is not a rigid playbook, but the ability to adapt, pivot, and outmaneuver new turns in the road.

That’s the reality of preparing for retirement in 2026. The year brings not just fresh opportunities, but also an array of uncertain detours: higher contribution limits, altered tax breaks, changes to health benefits. Each development shapes the landscape of how diligently—and wisely—you can safeguard your savings and manage your expenses.

According to Joon Um, a seasoned CFP® and tax professional at Secure Tax & Accounting, anticipating these pivots—rather than scrambling after them—remains the surest path to security. “Planning ahead matters more than reacting at the last minute,” he notes.

Whether you’re minutes from the finish line or just building momentum, paying attention to every new rule for 2026 could make the difference between a smooth landing and future headaches.

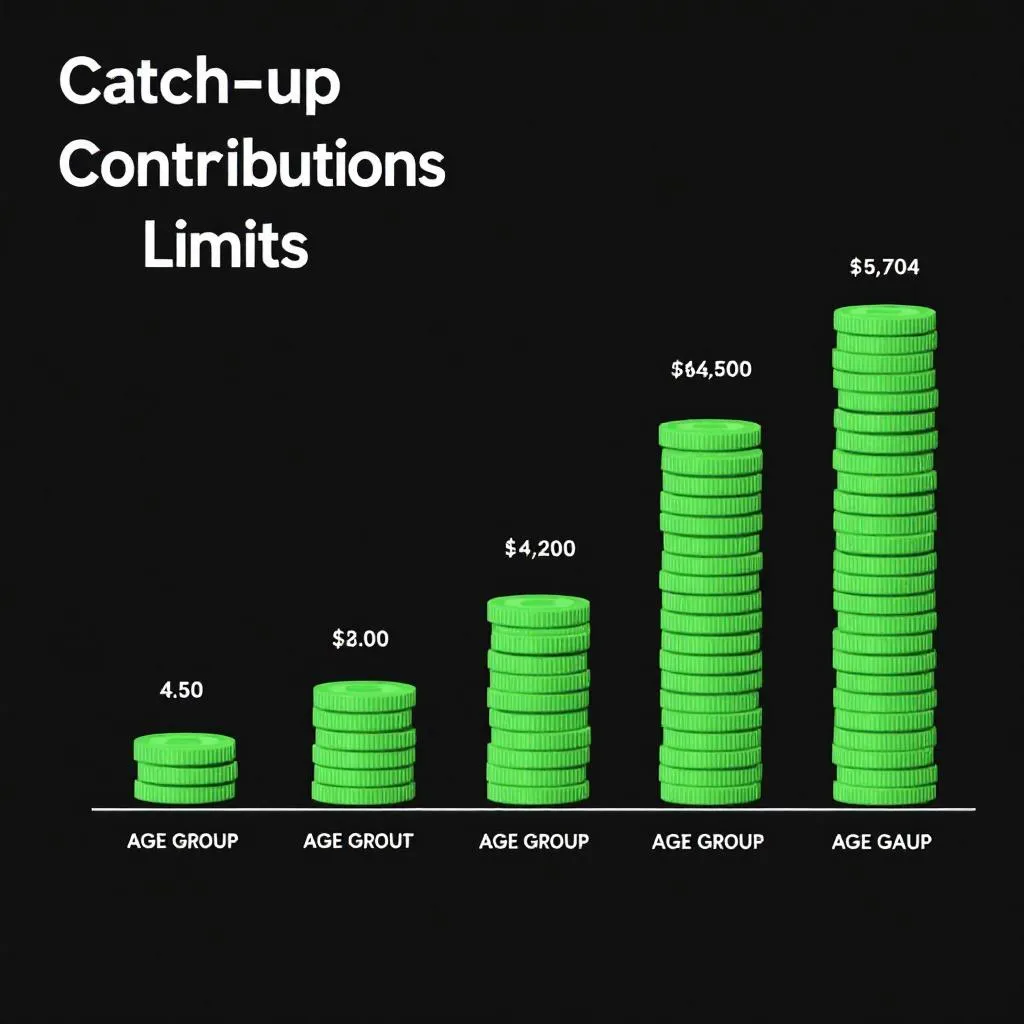

Near-retirees have reasons to celebrate: the cap on 401(k) contributions climbs to $24,500, and those 50-plus get an extra “catch-up” allowance—$8,000 more. For IRAs, the bar rises to $7,500, plus a $1,100 kicker for older savers. If you’re thinking about maxing out, there’s plenty more room.

But for high earners—those pulling in over $150,000—there’s a new caveat: catch-up contributions to your 401(k) after 2026 go in as Roth, not pre-tax. That tweak can throw a wrench into your tax plans, so strategize accordingly.

And for people aged 60–63? The “super catch-up” debuts, letting you sock away as much as $11,250 extra. Kate Feeney, vice president at Summit Place Financial Advisors, observes this could allow someone to funnel up to $35,750 each year—over $140,000 in four years—just before retirement sets in. For those who once shortchanged their retirement to meet other goals, this is a rare, late-game bonus.

But don’t be fooled: no one formula fits everyone. The oft-cited “rule of 25”—stashing 25 times your expected annual spending—offers a rough target. Yet, every retirement is idiosyncratic, as individual as the dreams behind it.

2. The return of the health care subsidy trapdoor

For those quitting work before Medicare, 2026 brings a nasty surprise. ACA (Affordable Care Act) premium subsidies revert to pre-2021 standards, eliminating credits entirely for couples earning over about $84,600 (that’s 400% of the poverty level). Fall a dollar over, and suddenly your insurance premiums could skyrocket.

This infamous “subsidy cliff” means that managing your taxable income becomes as much a health care issue as a tax one. Jeremy Keil, a financial planner, urges vigilance: “Be careful which accounts you draw from, and how much.” Even a modest income bump may cost you dearly in lost subsidies—sometimes tens of thousands in extra costs.

So, if you’re eyeing early retirement, recognize: what you pull from which bucket isn’t just about IRS brackets anymore. It’s about affording to stay healthy.

3. Medicare costs keep climbing

Past 65, unpredictability persists. The monthly premium for Medicare Part B jumps to nearly $203, up nearly 10% in a single year. Deductibles aren’t spared either.

Although these increases might seem minor, they erode budgets over the years, especially for those whose health care bills don’t stop at insurance. These slow, steady hikes—multiplied by the fact that living into our 90s is becoming the norm—make future-proofing your savings mission-critical.

4. Higher standard deduction, tailored senior tax breaks

Taxes offer some breathing room. For 2025 returns, couples can claim a $31,500 standard deduction, with a further boost for seniors. Plus, those over 65 could see a unique, though temporary, deduction of $6,000 each ($12,000 for couples), phased out at higher income levels and likely expired after 2028.

But don’t let tax perks steer every decision. As Keil warns, obsessing over deductions sometimes leads retirees to miss out on better long-term moves, like Roth conversions or necessary withdrawals.

5. Tweaks to charitable giving

Donor rules are shifting too. Non-itemizers can now write off up to $2,000 in cash gifts as a deduction, but for itemizers, things get less generous: the initial 0.5% of donations is no longer deductible, with no way to recoup it later. Clark Randall, a director at Creekmur Wealth Advisors, cautions: “You can’t have it both ways—itemizing and taking the ‘above-the-line’ deduction.”

For retirees 70½ and up, the limit for qualified charitable distributions (QCDs) grows to $111,000 per person, helping satisfy RMDs while reducing taxable income—a move that might tempt anyone embracing the “spend-down” approach.

Seeing the full playing field

All these federal shifts are significant, but real retirement planning runs deeper. Rules overlap with lived realities—state tax quirks, rising insurance costs, family needs, lifestyle changes. As Um sums up: “2026 isn’t about one grand change. It’s about keeping every lever—taxes, health, income, spending—in alignment.”

The real “rule” of 2026? Retirement is a living, breathing process. Your playbook is never finished. Adapt constantly, and you’ll stay a step ahead.