April 23, 2026

By Maurie Backman

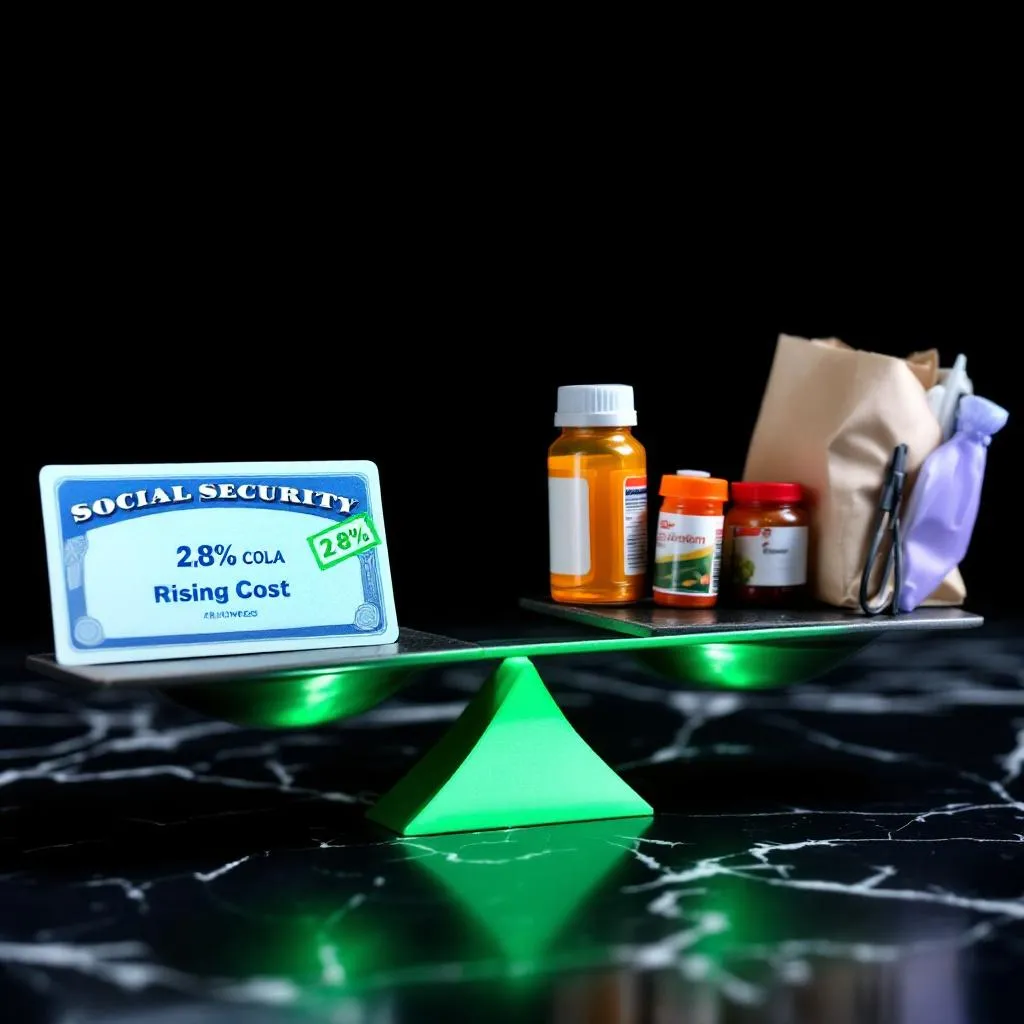

The start of a new year usually brings some measure of hope to those living on a fixed income. When Social Security announces its annual cost-of-living adjustment (COLA), countless retirees scan the news for details, weighing how that seemingly small number will ripple through their daily expenses. For 2026, the official COLA clocks in at 2.8 percent. On paper, it should feel like a modest cushion—a buffer against rising prices. But step into the real world, and that percentage quickly loses heft.

Picture an older couple in a quiet suburb, counting on Social Security for most of their income. Each month, their benefits will in fact inch up. Yet, the groceries they depend on—fresh vegetables, milk, bread, maybe the occasional treat—have all crept higher in price over the past year at a rate the COLA hasn’t quite caught. Prescription drugs, the bills that can’t be sacrificed, keep stealing a bigger chunk of their pay. Phone calls between friends inevitably lead to a shared refrain: “Everything costs more, but our money stays the same.”

Let’s break it down. The government calculates COLAs by tracking the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). It’s a blunt tool, measuring inflation based on the spending habits of working Americans—not retirees. Medical care, for example, weighs less in this formula than it probably should for the average senior. Housing and utility costs, which can swallow a huge fraction of a retiree’s budget, often shift in ways the index only weakly reflects. So, while Congress aims for fairness, the adjustment lands short for many.

The numbers might look encouraging at first. If you receive $1,800 a month in Social Security this year, a 2.8 percent COLA translates to an extra $50 or so per month in 2026. Welcome, sure, but what does fifty dollars do against rent spikes, steeper utility charges, or a health insurance premium that refuses to sit still? Some expenses—medications, dental work, even the simple luxury of heating a home in January—rise much faster than the COLA shadow can stretch.

For some, the shortfall feels especially stark. Seniors who rent face almost relentless increases, and affordable housing grows scarce. Food costs haven’t relented, as anyone who’s pushed a half-full cart through the checkout can testify. Add in medical appointments, co-pays, the price of hearing aids or glasses—all vital, and all expensive. The COLA doesn’t notice these nuances; it’s a one-size-fits-all answer to a complex equation.

The frustration is palpable, especially among those who spent decades at work, trusting that Social Security would provide dignity and steadiness in their later years. Many now must revisit their budgets, trimming away not just luxuries but also necessities—maybe a favorite weekly meal, or even a prescription filled at half the recommended dose. Adult children worry or offer help; pride and practicality wrestle in the open.

Policymakers occasionally float alternatives. Some argue for using the Consumer Price Index for the Elderly (CPI-E), which tracks costs more relevant to seniors’ lives. It’s a genteel debate in the halls of Congress, but for now, nothing changes. Year after year, retirees wait for COLA announcements, and year after year, the percentage lags behind real-life inflation.

Retirement, as imagined by previous generations, meant peace—a time to breathe. Instead, for too many, it’s become a careful balancing act. COLA is supposed to lend support, but its reach grows shorter with every bill slipped under the door.

So as 2026 draws near, that 2.8 percent uptick is hardly cause for celebration. It is, at best, a nod to inflation, not a solution. Retirees deserve more than relief in small increments; they deserve adjustments that meet the real cost of growing old in America.